The Quantum Computing Market – State of Play

The Quantum Computing Market – State of Play

Whither commercial quantum computing?

Happy 2024 to you! I hope the year is off to a great start.

This article is a little different: instead of discussing something technical, we’ll take a look at something more business-oriented; namely, the quantum computing market. This topic is interesting because while quantum computing is not yet a fully-matured technology, the evolution of the market and the evolution of the technology influence one another. For example, fears of a “quantum winter” (where funding dries up) might influence the decisions of leaders of quantum computing companies as to how to allocate people and capital to weather the downturn. In turn, this influences the direction of research. And in the other direction, advances in the research can help accelerate the market-readiness of the technology.

This article will be using data compiled by Hyperion Research, LLC and which was presented by Bob Sorenson of Hyperion at Q2B 2023 in Silicon Valley. The slides from Rob’s talk are available here, courtesy of the QED-C. (QCWare team, it would be great if the talk itself is made available on your YouTube channel at some point! See here.)

Below is a set of figures from a subset of the slides based on which ones seemed most relevant. The figures present the slides in their entirety, with no edits or adjustments, and are captioned as Figure X [Slide Y]: Caption. Again, all credit goes to Hyperion for their efforts in conducting the survey which led to these results!

Let’s dive in.

Overview of Survey Results

It’s quite astonishing the market is “only” about $150M shy of $1B in size, especially given that to date, no end-users are using gate-based quantum computers as part of their regular business operations. And especially astonishing when considering that it was only 7 years ago that access to such quantum computers was made publicly-available. That the market could grow by 2026 to ~$1.5B seems reasonable, in my opinion, especially as the hardware and software advances and more end-users are onboarded.

The increase in use case exploration by the high-performance computing (HPC) community is encouraging. There have been partnerships between HPC centers announced in the EU and Japan, and hopefully more will happen in the coming years across the globe. Finding ways for quantum computers to seamlessly integrate into HPC infrastructure, so that HPC becomes “quantum-aware” is going to be an incredible opportunity for the future of HPC!

That R&D in quantum is anticipated to be the most attractive end-user in 2026 for about 50% of suppliers is surprising. I would have figured that number would be smaller, as suppliers would want to go after more and more commercially-relevant end-users.

ChatGPT is the quantum-killer? Not quite, but given everything in the media these days about generative AI and large language models, it’s not surprising that many end-users are finding themselves having to weigh doing projects in quantum against working on genAI or LLMs.

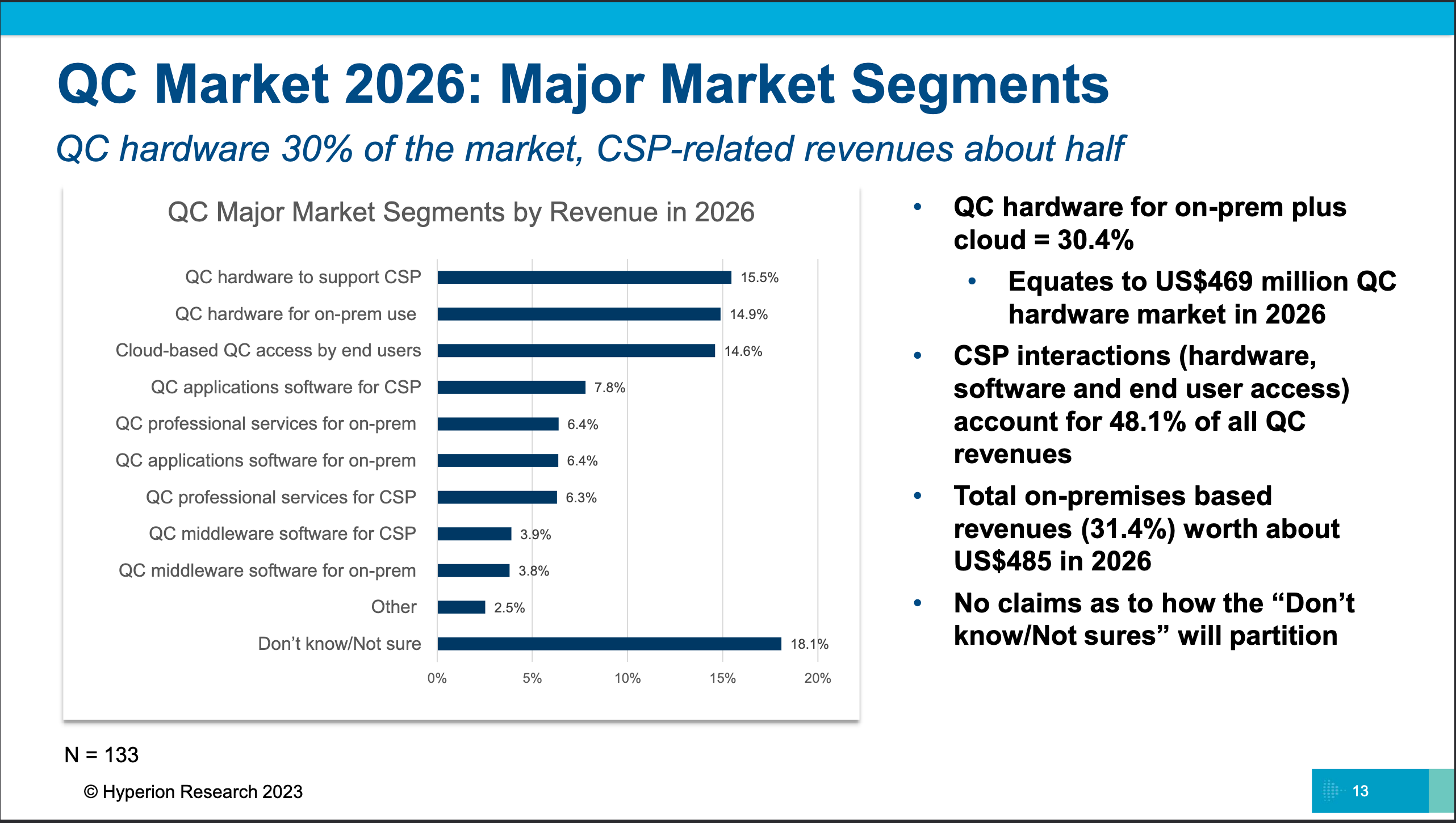

Quantum Computing Market Segments

Of all the ways to generate revenue, providing access to hardware is far and away the biggest share of the pie. That’s pretty obvious, in a way – without the hardware, you can’t run anything! What is interesting is that all 3 ways of providing access (which I interpret as “selling hardware to cloud providers”, “selling hardware for an on-premise installation”, or “selling cloud-based access to your hardware”) are roughly comparable in terms of share.

Professional services accounts for a good share of the pie (about 12.5%, or $187.5M). Consultants and the professional services class, take note!

In time, I’d expect the revenues from ‘middleware’ to take a larger share of the pie as quantum continues to be integrated into HPC systems.

Quantum Algorithms and Access to Hardware

(The inset plot above is from last year’s survey, slide 15.)

It’s not so clear to me what “Cybersecurity” would mean in this context, since it’s unlikely near-future quantum computers would be capable of breaking cryptography. I suppose it could mean using quantum computers for cybersecurity-relevant tasks (such as network monitoring, intrusion detection, etc.). If this category does mean cryptography, that it comes in with as high a percentage as it does is surprising to me.

Setting aside “Other”, “Don’t know”, and “Cybersecurity”, almost 2/3 of the pie consists of 4 categories. Three of these (Modeling/Simulation, Optimization, AI (ML & DL)) are pretty standard when talking about quantum applications. For the “Monte Carlo Processes” category, I would assume that refers to risk analysis (or risk-analysis-adjacent) calculations.

The growth in the “Other” category is a bit odd, and perhaps is worth diving into.

Quantum is growing up in the cloud era, and it shows! That access via the cloud continues to dominate isn’t so surprising – standing up and maintaining highly-reliable systems is quite an engineering challenge. This said, as the integration with HPC continues, I’d expect the share for on-premises capability to increase in future surveys.

End-users: which are the most prominent, and what do they expect?

One nit-picking point: this slide seems to pull apart things which are actually related. For example, how is ‘cybersecurity’ different from ‘defense’, or any commercially-relevant category? This could make drawing conclusions difficult.

That some of the most promising categories involve some flavor of chemistry (chemistry itself, pharma, biosciences) isn’t too surprising. What is surprising is the drop in the finance industry: many financial services companies are aggressively investing in quantum. That said, coming down only a few slots doesn’t necessarily portend the end of that sector.

Some of the most prominent end-user companies in quantum computing fall into categories which show up lower in the ranking. I’m not exactly sure how to understand the mis-match.

It’s encouraging to see “Defense” in the upper half of the list. In the US, the Department of Defense has a long history of funding quantum information science research, and there are some really exciting activities taking place via the Navy and the Air Force over the past few years. Last year, as part of the FY 2024 National Defense Authorization Act, Congress authorized DoD to pursue a pilot program on near-term quantum computing applications (Sec 231). I hope that program bears much good fruit, and lays solid foundations for the DoD to get quantum-ready!

The top 4 perceptions could be summed up as “I wanted to be prepared and get ready.”. It’s especially encouraging that respondents say they aren’t expecting to deploy or otherwise use what they come up with in the near-term. End-users really need to manage internal expectations well, lest someone feels like they were sold snake oil.

That reducing computation cost or energy usage ranks low isn’t too surprising – for now, end-users just want to have the competencies and skills to take advantage of quantum as it matures. Of course, as quantum computing systems scale, us suppliers are going to need to innovate to keep system bring-up and operations costs/energy low. (As noted in a prior article, new and more energy-efficient approaches to controlling qubits are going to be needed.) What would be interesting to see is whether larger market forces around sustainability eventually drive end-users to prioritize quantum as a result.

Wrap-up

As noted in the introduction, the figures above do not cover all the slides. If you are curious about the demographics of suppliers, have a strong curiosity about quantum winter, or have thoughts about what the rise of generative AI might do to the market, check out the talk itself.

Overall, the survey paints a picture appropriate to the talk’s title: the quantum computing market is “Robust and on the Rise”. Of course there are no guarantees, but for now, the future of quantum computing’s market viability looks bright.

Ask and ye shall receive: Bob's presentation is on YouTube at https://www.youtube.com/watch?v=24ECyNdemc0